How to test for the existence of a unit root in EViews – Stationarity of a Series

How to test for the existence of a unit root in EViews – Stationarity of a Series

To test for the existence of a unit root in EViews and the stationarity of a series, you can use the following steps:

Unit Root Testing in EViews:

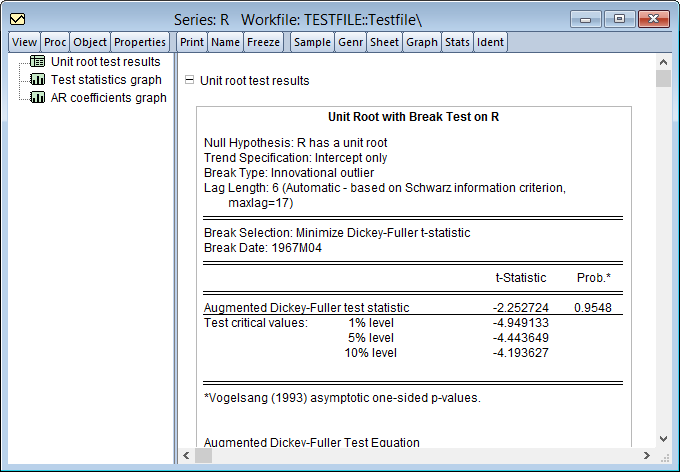

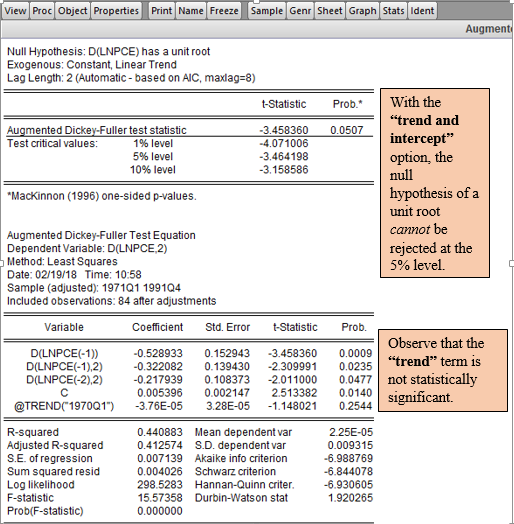

EViews provides a variety of unit root testing tools, including the Augmented Dickey-Fuller (ADF) test, HEGY test, Canova and Hansen test, and Variance Ratio tests

You can run a unit root test by specifying the series and the test type in EViews, such as the ADF test, Phillips-Perron test, or other relevant tests

How to test for the existence of a unit root in EViews – Stationarity of a Series

Interpreting the Results:

When interpreting the results of a unit root test, you should consider the test statistic, p-value, and critical values. For example, if the test statistic is less than the critical value, you may reject the null hypothesis of a unit root and conclude that the series is stationary

Stationarity Testing:

To test for stationarity, you can use correlograms and unit root tests. If the unit root test indicates the presence of a unit root, the series is non-stationary. Conversely, if the test suggests the absence of a unit root, the series is stationary

It’s important to ensure that the series is stationary before performing further analysis, such as time series modeling or forecasting.

How to test for the existence of a unit root in EViews – Stationarity of a Series

Additional Resources:

You can refer to EViews tutorials and resources available on platforms like YouTube and EViews forums for step-by-step guidance on conducting unit root tests and checking for stationarity in EViews

By following these steps and considering the test results, you can effectively test for the existence of a unit root and the stationarity of a series in EViews.

Choose from hundreds of experts who can assist you in completing your undergraduate dissertation! Prices start at $10 per page, with potential discounts for longer orders or extended deadlines

Master’s dissertation

If you are in the process of completing a Master’s degree, we can provide you with an experienced writer to finish your dissertation. We strive to offer a quick turnaround on tailored papers at an affordable price, starting at $10.30 per page.

Ph.D. or doctoral dissertation

Hire from among our most skilled experts to save your time and ease your workload. Prices for Ph.D. assistance start at $10.60 per page.